Regularization Techniques

Regularization Methods Example 1.1¶

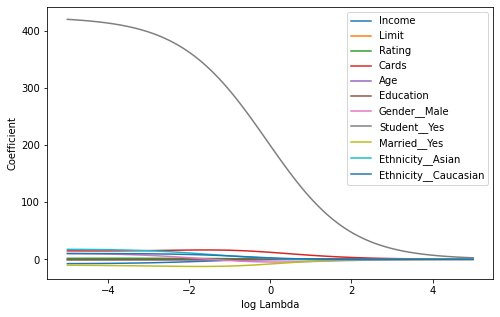

In the figure below, the ridge regression coefficient estimates for the Credit data set are displayed. Each curve corresponds to the ridge regression coefficient estimate for one of the ten variables, plotted as a function of . For example, the blue solid line represents the ridge regression estimate for the income coefficient, as is varied. At the extreme left-hand side of the plot, is essentially zero, and so the corresponding ridge coefficient estimates are the same as the usual least squares estimates. But as increases, the ridge coefficient estimates shrink towards zero. When is extremely large, then all of the ridge coefficient estimates are basically zero; this corresponds to the null model that contains no predictors.

While the ridge coefficient estimates tend to decrease in aggregate as increases, individual coefficients, such as rating and income, may occasionally increase as increases.

Sklearn version:¶

import pandas as pd

import numpy as np

from sklearn.linear_model import Ridge

import warnings

warnings.filterwarnings("ignore")

# Load data

df = pd.read_csv('Regularization Techniques/data/Credit.csv', index_col="Unnamed: 0")

# Convert Categorical variables

df = pd.get_dummies(data=df, drop_first=True,

prefix=('Gender_', 'Student_',

'Married_', 'Ethnicity_'))

# Define target and predictors

x = df.drop(columns='Balance')

y = df['Balance']

# Model for different lambda

n = 100

lambda_ = np.exp(np.linspace(-5, 5, n))

params = pd.DataFrame(columns=x.columns)

for i in range(n):

reg = Ridge(alpha=lambda_[i], normalize=True)

reg = reg.fit(x, y)

params.loc[np.log(lambda_[i]), :] = reg.coef_import matplotlib.pyplot as plt

# Plot

fig = plt.figure(figsize=(8, 5))

ax = fig.add_subplot(1, 1, 1)

params.plot(ax=ax)

plt.xlabel("log Lambda")

plt.ylabel("Coefficient")

plt.legend()

plt.show()

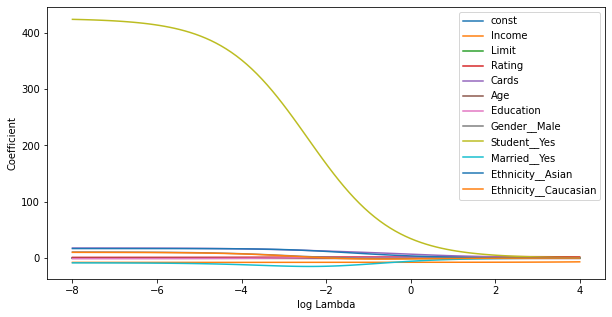

Statsmodels¶

Statsmodels seems to have some scaling wrt Alpha, which makes the results difficult to compare with R. (Allthough generally correct) Furthermore, the implementation seems to be incomplete, for example the summary function is missing.

import pandas as pd

import numpy as np

import statsmodels.api as sm

from sklearn import preprocessing

# Load data

df = pd.read_csv('Regularization Techniques/data/Credit.csv', index_col="Unnamed: 0")

# Convert Categorical variables

df = pd.get_dummies(data=df, drop_first=True,

prefix=('Gender_', 'Student_',

'Married_', 'Ethnicity_'))

# Define target and predictors

x = df.drop(columns='Balance')

x = sm.add_constant(x)

y = df['Balance']

# Scale to 0 mean:

scaler = preprocessing.StandardScaler(with_std=False).fit(x)

x_scaled = scaler.transform(x)

# Model for different lambda

n = 100

lambda_ = np.linspace(-8, 4, n)

params = pd.DataFrame(columns=x.columns)

for lam in lambda_:

model = sm.OLS(y, x_scaled)

model = model.fit_regularized(alpha=np.exp(lam), L1_wt=0)

params.loc[lam, :] = model.paramsimport matplotlib.pyplot as plt

# Plot

fig = plt.figure(figsize=(10, 5))

ax = fig.add_subplot(1, 1, 1)

params.plot(ax=ax)

plt.xlabel("log Lambda")

plt.ylabel("Coefficient")

plt.legend()

plt.show()

Regularization Methods Example 1.2:¶

In the following, we will discuss the function sklearn.linear_model.Ridge() in depth. Firstly, note that the qualitative predictors in x have to be transformed into dummy variables. The flag normalize = True makes sure that the predictors are mean centred and scaled to unit variance. When comparing to R, note that the implementation is slightly different, which makes it hard to compare coefficients as a function of lambda. The optimal solution however, will generally be the same.

We will now perform ridge regression in order to predict Balance in the Credit data set.

import pandas as pd

import numpy as np

from sklearn.linear_model import Ridge

import warnings

warnings.filterwarnings("ignore")

# Load data

df = pd.read_csv('Regularization Techniques/data/Credit.csv', index_col="Unnamed: 0")

# Convert Categorical variables

df = pd.get_dummies(data=df, drop_first=True,

prefix=('Gender_', 'Student_',

'Married_', 'Ethnicity_'))

# Define target and predictors

x = df.drop(columns='Balance')

y = df['Balance']

# Fit model:

lambda_ = 100

reg = Ridge(alpha=lambda_, normalize=True)

reg = reg.fit(x, y)

# Coefficient and corresponding predictors

coef = np.round(reg.coef_, 3)

# coef = scaler.inverse_transform(coef)

x_cols = x.columns.valuesWe expect the coefficient estimates to be much smaller, in terms of norm, when a large value of is used, as compared to when a small value of is used. These are the coefficients when , along with their norm:

print(pd.DataFrame(data={'Feature': x_cols,

'Coefficient':coef}),

'\n\nl2-norm:', np.sqrt(np.sum(coef**2))) Feature Coefficient

0 Income 0.006

1 Limit 0.000

2 Rating 0.003

3 Cards 0.029

4 Age 0.000

5 Education -0.001

6 Gender__Male -0.020

7 Student__Yes 0.396

8 Married__Yes -0.005

9 Ethnicity__Asian -0.010

10 Ethnicity__Caucasian -0.003

l2-norm: 0.3977901456798547

In contrast, here are the coefficients when , along with their norm. Note the much larger norm of the coefficients associated with this smaller value of .

# Fit model:

lambda_ = 50

reg = Ridge(alpha=lambda_, normalize=True)

reg = reg.fit(x, y)

# Coefficient and corresponding predictors

coef = np.round(reg.coef_, 3)

x_cols = x.columns.values

print(pd.DataFrame(data={'Feature': x_cols,

'Coefficient':coef}),

'\n\nl2-norm:', np.sqrt(np.sum(coef**2))) Feature Coefficient

0 Income 0.112

1 Limit 0.003

2 Rating 0.049

3 Cards 0.563

4 Age -0.002

5 Education -0.021

6 Gender__Male -0.379

7 Student__Yes 7.773

8 Married__Yes -0.123

9 Ethnicity__Asian -0.183

10 Ethnicity__Caucasian -0.052

l2-norm: 7.806846994786052

The standard least squares coefficient estimates are scale equivariant: multiplying a predictor variable by a constant simply leads to a scaling of the least squares coefficient estimates by a factor of . In other words, regardless of how the th predictor is scaled, will remain the same. In contrast, the ridge regression coefficient estimates can change substantially when multiplying a given predictor by a constant. For instance, consider the income variable, which is measured in dollars. One could reasonably have measured income in thousands of dollars, which would result in a reduction in the observed values of income by a factor of 1000. Now due to the sum of squared coefficients in the ridge regression formulation equation, such a change in scale will not simply cause the ridge regression coefficient estimate for income to change by a factor of 1000. In other words, will depend not only on the value of , but also on the scaling of the th predictor. In fact, the value of may even depend on the scaling of the other predictors. Therefore, it is best to apply ridge regression after standardizing the predictors.

Note that by default, the Ridge() function does not standardizes the variables. To turn on scaling, use the argument normalize = True.

Regularization Methods Example 2.3:¶

In order to fit a lasso model, we use the sklearn.linear_model.Lasso() function, which behaves very similar to the Ridge() function.

import pandas as pd

import numpy as np

from sklearn.linear_model import Lasso

import warnings

warnings.filterwarnings("ignore")

# Load data

df = pd.read_csv('Regularization Techniques/data/Credit.csv', index_col="Unnamed: 0")

# Convert Categorical variables

df = pd.get_dummies(data=df, drop_first=True,

prefix=('Gender_', 'Student_',

'Married_', 'Ethnicity_'))

# Define target and predictors

x = df.drop(columns='Balance')

y = df['Balance']

# Fit model:

lambda_ = 5

reg = Lasso(alpha=lambda_, normalize=True)

reg = reg.fit(x, y)

# Coefficient and corresponding predictors

coef = np.round(reg.coef_, 3)

x_cols = x.columns.valuesWe expect the coefficient estimates to be much smaller, in terms of norm, when a large value of is used, as compared to when a small value of is used. These are the coefficients when , along with their norm:

print(pd.DataFrame(data={'Feature': x_cols,

'Coefficient':coef}),

'\n\nl2-norm:', np.sqrt(np.sum(coef**2))) Feature Coefficient

0 Income -0.000

1 Limit 0.010

2 Rating 1.769

3 Cards 0.000

4 Age -0.000

5 Education 0.000

6 Gender__Male -0.000

7 Student__Yes 65.438

8 Married__Yes -0.000

9 Ethnicity__Asian 0.000

10 Ethnicity__Caucasian -0.000

l2-norm: 65.46190728202167

In contrast, here are the coefficients when , along with their norm. Note the much higher norm of the coefficients associated with this lower value of .

# Fit model:

lambda_ = 0.5

reg = Lasso(alpha=lambda_, normalize=True)

reg = reg.fit(x, y)

# Coefficient and corresponding predictors

coef = np.round(reg.coef_, 3)

x_cols = x.columns.values

print(pd.DataFrame(data={'Feature': x_cols,

'Coefficient':coef}),

'\n\nl2-norm:', np.sqrt(np.sum(coef**2))) Feature Coefficient

0 Income -6.491

1 Limit 0.145

2 Rating 1.508

3 Cards 9.417

4 Age -0.236

5 Education -0.000

6 Gender__Male 0.000

7 Student__Yes 387.093

8 Married__Yes -0.000

9 Ethnicity__Asian 0.000

10 Ethnicity__Caucasian 0.000

l2-norm: 387.26496666236153

As we can observe, several coefficients have become zero. The larger the value of the more coefficients become zero. Variable selection thus is generically implemented in the lasso.

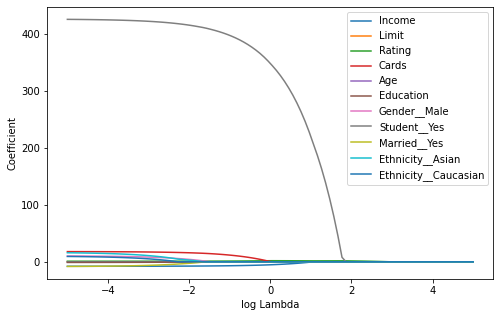

Figure¶

import matplotlib.pyplot as plt

# Model for different lambda

n = 100

lambda_ = np.exp(np.linspace(-5, 5, n))

params = pd.DataFrame(columns=x.columns)

for i in range(n):

reg = Lasso(alpha=lambda_[i], normalize=True)

reg = reg.fit(x, y)

params.loc[np.log(lambda_[i]), :] = reg.coef_

# Plot

fig = plt.figure(figsize=(8, 5))

ax = fig.add_subplot(1, 1, 1)

params.plot(ax=ax)

plt.xlabel("log Lambda")

plt.ylabel("Coefficient")

plt.legend()

plt.show()

Regularization Methods Example 2.4:¶

We now split the samples of the Credit data set into a training set and a test set in order to estimate the test error of ridge regression and the lasso. The splitting can be easily achieved using the train_test_split() function from sklearn.model_selection. We first set a random seed so that the results obtained will be reproducible.

import pandas as pd

import numpy as np

from sklearn.linear_model import Ridge

from sklearn.model_selection import train_test_split

# Load data

df = pd.read_csv('Regularization Techniques/data/Credit.csv', index_col="Unnamed: 0")

# Convert Categorical variables

df = pd.get_dummies(data=df, drop_first=True,

prefix=('Gender_', 'Student_',

'Married_', 'Ethnicity_'))

# Define target and predictors

x = df.drop(columns='Balance')

y = df['Balance']

# Split in test and train set

np.random.seed(10)

x_train, x_test, y_train, y_test = train_test_split(x, y,

test_size=0.5)We now split the samples of the Credit data set into a training set and a test set in order to estimate the test error of ridge regression and the lasso. The splitting can be easily achieved using the train_test_split() function from sklearn.model_selection. We first set a random seed so that the results obtained will be reproducible.

import warnings

warnings.filterwarnings("ignore")

# Model for lambda=4

params = pd.DataFrame(columns=x.columns)

lambda_ = 4

# Fit model:

reg = Ridge(alpha=lambda_, normalize=True)

reg = reg.fit(x_train, y_train)

# Coeficient and coresponding predictors

coef = np.round(reg.coef_, 3)

x_cols = x.columns.values

print(pd.DataFrame(data={'Feature': x_cols,

'Coefficient':coef}))

# Predict and calculate MSE on test-set

y_pred = reg.predict(x_test)

MSE = np.mean((y_pred - y_test)**2)

print("\nMSE:", np.round(MSE, 1)) Feature Coefficient

0 Income 0.656

1 Limit 0.028

2 Rating 0.418

3 Cards 4.490

4 Age -0.323

5 Education -0.251

6 Gender__Male -8.147

7 Student__Yes 99.132

8 Married__Yes 3.622

9 Ethnicity__Asian -1.485

10 Ethnicity__Caucasian 1.972

MSE: 116077.3

The test MSE is 116077.3. Note that if we had instead simply fit a model with just an intercept, we would have predicted each test observation using the mean of the training observations. In that case, we could compute the test set MSE like this:

MSE = np.mean((np.mean(y_train) - y_test)**2)

print("MSE:", np.round(MSE, 1))MSE: 214872.8

We could also get the same result by fitting a ridge regression model with a very large value of .

# Model for lambda=inf

lambda_ = 1e10

# Fit model:

reg = Ridge(alpha=lambda_, normalize=True)

reg = reg.fit(x_train, y_train)

# Coeficient and coresponding predictors

coef = np.round(reg.coef_, 3)

x_cols = x.columns.values

print(pd.DataFrame(data={'Feature': x_cols,

'Coefficient':coef}))

# Predict and calculate MSE on test-set

y_pred = reg.predict(x_test)

MSE = np.mean((y_pred - y_test)**2)

print("\nMSE:", np.round(MSE, 1)) Feature Coefficient

0 Income 0.0

1 Limit 0.0

2 Rating 0.0

3 Cards 0.0

4 Age -0.0

5 Education -0.0

6 Gender__Male -0.0

7 Student__Yes 0.0

8 Married__Yes 0.0

9 Ethnicity__Asian -0.0

10 Ethnicity__Caucasian 0.0

MSE: 214872.8

So fitting a ridge regression model with leads to a much lower test MSE than fitting a model with just an intercept. We now check whether there is any benefit to performing ridge regression with instead of just performing least squares regression. Recall that least squares is simply ridge regression with .

# Model for lambda=0

lambda_ = 0

# Fit model:

reg = Ridge(alpha=lambda_, normalize=True)

reg = reg.fit(x_train, y_train)

# Coeficient and coresponding predictors

coef = np.round(reg.coef_, 3)

x_cols = x.columns.values

print(pd.DataFrame(data={'Feature': x_cols,

'Coefficient':coef}))

# Predict and calculate MSE on test-set

y_pred = reg.predict(x_test)

MSE = np.mean((y_pred - y_test)**2)

print("\nMSE:", np.round(MSE, 1)) Feature Coefficient

0 Income -7.666

1 Limit 0.168

2 Rating 1.421

3 Cards 20.156

4 Age -0.333

5 Education 0.942

6 Gender__Male -13.405

7 Student__Yes 455.791

8 Married__Yes -10.613

9 Ethnicity__Asian 18.956

10 Ethnicity__Caucasian 27.706

MSE: 10730.6

The MSE resulting form Ridge regression with is larger than the MSE resulting from least squares which is not surprising since we have arbitrarily chosen .

In general, instead of arbitrarily choosing , it would be better to use cross-validation to choose the tuning parameter .

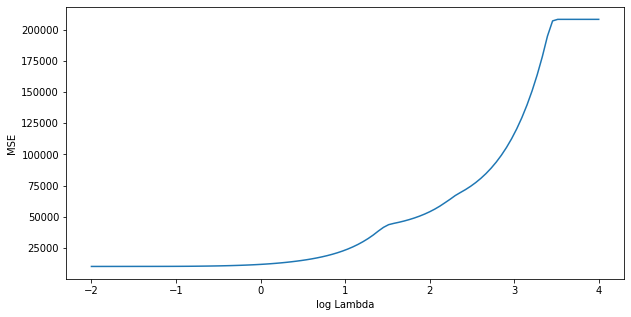

Regularization Methods Example 2.5:¶

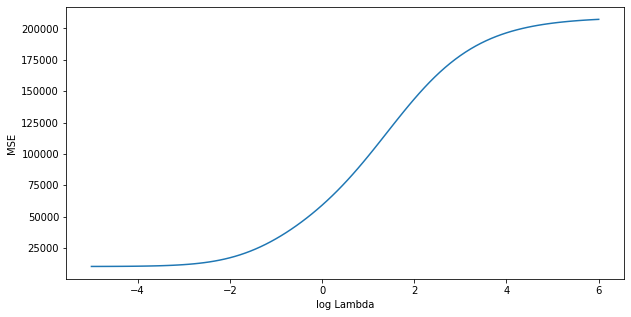

We can do this using the RidgeCV() function. By default, the number of folds equals the number of observations (leave-one-out), but this can be changed using the cv setting.

from sklearn.linear_model import RidgeCV

import matplotlib.pyplot as plt

n=100

lambda_ = np.exp(np.linspace(-5, 6, n))

# Fit model:

reg = RidgeCV(alphas=lambda_, store_cv_values=True, normalize=True)

reg = reg.fit(x_train, y_train)

# Plot

fig = plt.figure(figsize=(10, 5))

ax = fig.add_subplot(1, 1, 1)

ax.plot(np.log(lambda_), np.mean(reg.cv_values_, axis=0))

plt.xlabel("log Lambda")

plt.ylabel("MSE")

plt.show()

print("Best Lambda:", np.round(reg.alpha_, 3))Best Lambda: 0.007

Therefore, we see that the value of that results in the smallest cross-validation error is 0.007. What is the test MSE associated with this value of ?

# Predict and calculate MSE on test-set

y_pred = reg.predict(x_test)

MSE = np.mean((y_pred - y_test)**2)

print("MSE:", np.round(MSE, 1))MSE: 10894.1

Note that the best model is already returned by RidgeCV, we dont need to fit it again. The test MSE does represent an improvement over the test MSE we got using . Now we can also find the coefficients of the model.

# Coeficient and coresponding predictors

coef = np.round(reg.coef_, 3)

x_cols = x.columns.values

print(pd.DataFrame(data={'Feature': x_cols,

'Coefficient':coef})) Feature Coefficient

0 Income -7.406

1 Limit 0.139

2 Rating 1.803

3 Cards 18.373

4 Age -0.382

5 Education 0.984

6 Gender__Male -13.514

7 Student__Yes 451.436

8 Married__Yes -10.541

9 Ethnicity__Asian 20.025

10 Ethnicity__Caucasian 28.396

Regularization Methods Example 2.6¶

We now ask whether the lasso can yield either a more accurate or a more interpretable model than ridge regression.

from sklearn.linear_model import LassoCV

lambda_ = np.exp(np.linspace(-2, 4, n))

# Fit model:

reg = LassoCV(alphas=lambda_, normalize=True)

reg = reg.fit(x_train, y_train)

# Plot

fig = plt.figure(figsize=(10, 5))

ax = fig.add_subplot(1, 1, 1)

ax.plot(np.log(reg.alphas_), np.mean(reg.mse_path_, axis=1))

plt.xlabel("log Lambda")

plt.ylabel("MSE")

plt.show()

We can see from the coefficient plot that depending on the choice of tuning parameter, some of the coefficients will be exactly equal to zero. We now compute the associated test error.

# Predict and calculate MSE on test-set

y_pred = reg.predict(x_test)

MSE = np.mean((y_pred - y_test)**2)

print("Best Lambda:", np.round(reg.alpha_, 3), "\nMSE:", np.round(MSE, 1))Best Lambda: 0.135

MSE: 10538.4

This is substantially lower than the test set MSE of the null model, the test MSE of ridge regression with chosen by cross-validation, and very similar to least squares. Finally, we will have a look at the corresponding coefficients.

# Coeficient and coresponding predictors

coef = np.round(reg.coef_, 3)

x_cols = x.columns.values

print(pd.DataFrame(data={'Feature': x_cols,

'Coefficient':coef})) Feature Coefficient

0 Income -7.410

1 Limit 0.166

2 Rating 1.392

3 Cards 18.422

4 Age -0.277

5 Education 0.111

6 Gender__Male -8.978

7 Student__Yes 448.564

8 Married__Yes -4.421

9 Ethnicity__Asian 7.698

10 Ethnicity__Caucasian 17.483

In this example, all coefficients are different from zero.

Regularization Methods Example 2.7¶

Finally, we will discuss the Advertising data set.

import pandas as pd

import numpy as np

from sklearn.linear_model import LassoCV

from sklearn.model_selection import train_test_split

import warnings

warnings.filterwarnings("ignore")

# Load data

df = pd.read_csv('Regularization Techniques/data/Advertising.csv', index_col="Unnamed: 0")

# Define target and predictors

x = df.drop(columns='sales')

y = df['sales']

# Split in test and train set

np.random.seed(3)

x_train, x_test, y_train, y_test = train_test_split(x, y,

test_size=0.5)

# Fit model:

clf = LassoCV(normalize=True)

clf = clf.fit(x_train, y_train)

# Predict and calculate MSE on test-set

y_pred = clf.predict(x_test)

MSE = np.mean((y_pred - y_test)**2)

print("Best Lambda:", np.round(clf.alpha_, 3), "\nMSE:", np.round(MSE, 1))

# Coeficient and coresponding predictors

coef = np.round(clf.coef_, 3)

x_cols = x.columns.values

print(pd.DataFrame(data={'Feature': x_cols,

'Coefficient':coef}))Best Lambda: 0.014

MSE: 3.7

Feature Coefficient

0 TV 0.041

1 radio 0.183

2 newspaper -0.000

In this case, the lasso automatically omits the predictor variable newspaper.

Regularization Methods Example 4.1:¶

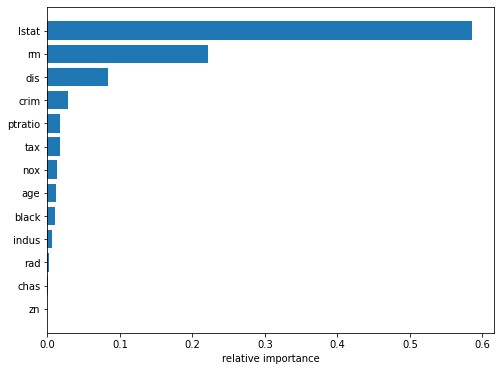

Here we use GradientBoostingRegressor() from sklearn.ensemble, to fit a boosted regression trees model to the Boston data set. The argument n_estimators=5000 indicates that we want 5000 trees, the option max_depth=4 limits the depth of each tree, and learning_rate=0.001 shrinks the contribution of each tree.

import pandas as pd

import numpy as np

from sklearn.model_selection import train_test_split

from sklearn.ensemble import GradientBoostingRegressor

# Load data

df = pd.read_csv('Regularization Techniques/data/Boston.csv', index_col=0)

# Define target and predictors

x = df.drop(columns='medv')

y = df['medv']

# Split in test and train set

np.random.seed(1)

x_train, x_test, y_train, y_test = train_test_split(x, y,

test_size=0.5)

# Fit model:

reg = GradientBoostingRegressor(n_estimators=5000, max_depth=4,

learning_rate=0.001)

reg = reg.fit(x_train, y_train)import matplotlib.pyplot as plt

# Feature Importances based on the impurity decrease

importance = reg.feature_importances_

features = x_train.columns.values

# Sort by importance

features = features[np.argsort(importance)]

importance = importance[np.argsort(importance)]

# plot

fig = plt.figure(figsize=(8, 6))

ax = fig.add_subplot(1, 1, 1)

ax.barh(features, importance)

ax.set_xlabel("relative importance")

plt.show()

We see that lstat and rm are by far the most important variables.

We now use the boosted model to predict medv on the test set:

from sklearn.metrics import mean_squared_error

# Predict

pred = reg.predict(x_test)

# MSE

MSE = mean_squared_error(y_test, pred)

print("MSE:", np.round(MSE, 3))MSE: 10.675

The test MSE obtained is 10.361; similar to the test MSE for random forests and superior to that for bagging. If we want to, we can perform boosting with a different value of the shrinkage parameter . The default value is 0.1, but this is easily modified. Here we take .

# Fit model with higher learning rate:

reg = GradientBoostingRegressor(n_estimators=5000, max_depth=4, learning_rate=0.2)

reg = reg.fit(x_train, y_train)

# Predict

pred = reg.predict(x_test)

# MSE

MSE = mean_squared_error(y_test, pred)

print("MSE:", np.round(MSE, 3))MSE: 10.228

In this case, using leads to a slightly lower test MSE than .

Regularization Methods Example 5.1¶

The sinking of the Titanic is one of the most infamous shipwrecks in history. On April 15, 1912, during her maiden voyage, the widely considered “unsinkable” RMS Titanic sank after colliding with an iceberg. Unfortunately, there weren’t enough lifeboats for everyone onboard, resulting in the death of 1502 out of 2224 passengers and crew.

While there was some element of luck involved in surviving, it seems some groups of people were more likely to survive than others. In this example, we ask you to build a predictive model that answers the question: “what sorts of people were more likely to survive?” using passenger data (i.e. name, age, gender, socio-economic class, etc).

In this example, we will compare the impurity-based feature importance of RandomForestClassifier with the permutation importance on the Titanic dataset using permutation_importance. We will show that the impurity-based feature importance can inflate the importance of numerical features.

Furthermore, the impurity-based feature importance of random forests suffers from being computed on statistics derived from the training dataset: the importances can be high even for features that are not predictive of the target variable, as long as the model has the capacity to use them to overfit.

This example shows how to use Permutation Importances as an alternative that can mitigate those limitations.

import matplotlib.pyplot as plt

import numpy as np

from sklearn.datasets import fetch_openml

from sklearn.ensemble import RandomForestClassifier

from sklearn.impute import SimpleImputer

from sklearn.inspection import permutation_importance

from sklearn.compose import ColumnTransformer

from sklearn.model_selection import train_test_split

from sklearn.pipeline import Pipeline

from sklearn.preprocessing import OneHotEncoderData Loading and Feature Engineering¶

Let’s use pandas to load a copy of the titanic dataset. The following shows how to apply separate preprocessing on numerical and categorical features.

We further include two random variables that are not correlated in any way with the target variable (survived):

random_numis a high cardinality numerical variable (as many unique values as records).random_catis a low cardinality categorical variable (3 possible values).

X, y = fetch_openml("titanic", version=1, as_frame=True, return_X_y=True)

rng = np.random.RandomState(seed=42)

X["random_cat"] = rng.randint(3, size=X.shape[0])

X["random_num"] = rng.randn(X.shape[0])

categorical_columns = ["pclass", "sex", "embarked", "random_cat"]

numerical_columns = ["age", "sibsp", "parch", "fare", "random_num"]

X = X[categorical_columns + numerical_columns]

X_train, X_test, y_train, y_test = train_test_split(X, y, stratify=y, random_state=42)

categorical_encoder = OneHotEncoder(handle_unknown="ignore")

numerical_pipe = Pipeline([("imputer", SimpleImputer(strategy="mean"))])

preprocessing = ColumnTransformer(

[

("cat", categorical_encoder, categorical_columns),

("num", numerical_pipe, numerical_columns),

]

)

rf = Pipeline(

[

("preprocess", preprocessing),

("classifier", RandomForestClassifier(random_state=42)),

]

)

rf.fit(X_train, y_train)Pipeline(steps=[('preprocess',

ColumnTransformer(transformers=[('cat',

OneHotEncoder(handle_unknown='ignore'),

['pclass', 'sex', 'embarked',

'random_cat']),

('num',

Pipeline(steps=[('imputer',

SimpleImputer())]),

['age', 'sibsp', 'parch',

'fare', 'random_num'])])),

('classifier', RandomForestClassifier(random_state=42))])Accuracy of the Model¶

Prior to inspecting the feature importances, it is important to check that the model predictive performance is high enough. Indeed there would be little interest of inspecting the important features of a non-predictive model.

Here one can observe that the train accuracy is very high (the forest model has enough capacity to completely memorize the training set) but it can still generalize well enough to the test set thanks to the built-in bagging of random forests.

It might be possible to trade some accuracy on the training set for a slightly better accuracy on the test set by limiting the capacity of the trees (for instance by setting min_samples_leaf=5 or min_samples_leaf=10) so as to limit overfitting while not introducing too much underfitting.

However let’s keep our high capacity random forest model for now so as to illustrate some pitfalls with feature importance on variables with many unique values.

print("RF train accuracy: %0.3f" % rf.score(X_train, y_train))

print("RF test accuracy: %0.3f" % rf.score(X_test, y_test))RF train accuracy: 1.000

RF test accuracy: 0.817

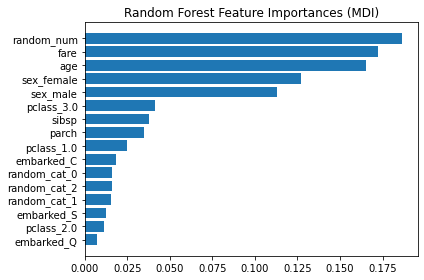

Tree’s Feature Importance from Mean Decrease in Impurity (MDI)¶

ohe = rf.named_steps["preprocess"].named_transformers_["cat"]

feature_names = ohe.get_feature_names(categorical_columns)

feature_names = np.r_[feature_names, numerical_columns]

tree_feature_importances = rf.named_steps["classifier"].feature_importances_

sorted_idx = tree_feature_importances.argsort()

y_ticks = np.arange(0, len(feature_names))

fig, ax = plt.subplots()

ax.barh(y_ticks, tree_feature_importances[sorted_idx])

ax.set_yticks(y_ticks)

ax.set_yticklabels(feature_names[sorted_idx])

ax.set_title("Random Forest Feature Importances (MDI)")

fig.tight_layout()

plt.savefig('rf_importance_mdi.png')

plt.show()

The impurity-based feature importance ranks the numerical features to be the most important features. As a result, the non-predictive random_num variable is ranked the most important!

This problem stems from two limitations of impurity-based feature importances:

impurity-based importances are biased towards high cardinality features;

impurity-based importances are computed on training set statistics and therefore do not reflect the ability of feature to be useful to make predictions that generalize to the test set (when the model has enough capacity).

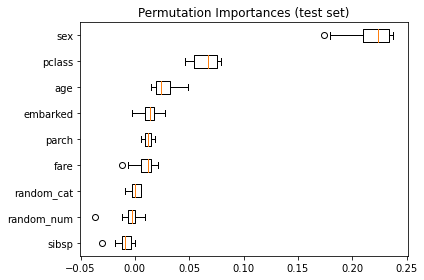

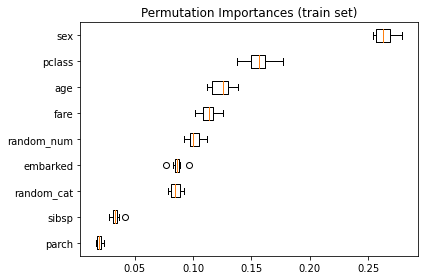

As an alternative, the permutation importances of rf are computed on a held out test set. This shows that the low cardinality categorical feature, sex is the most important feature.

Also note that both random features have very low importances (close to 0) as expected.

result = permutation_importance(rf, X_test, y_test, n_repeats=10, random_state=42)

sorted_idx = result.importances_mean.argsort()

fig, ax = plt.subplots()

ax.boxplot(

result.importances[sorted_idx].T, vert=False, labels=X_test.columns[sorted_idx]

)

ax.set_title("Permutation Importances (test set)")

fig.tight_layout()

plt.savefig('RT_Example_5_1_d.png')

plt.show()

It is also possible to compute the permutation importances on the training set. This reveals that random_num gets a significantly higher importance ranking than when computed on the test set. The difference between those two plots is a confirmation that the RF model has enough capacity to use that random numerical feature to overfit. You can further confirm this by re-running this example with constrained RF with min_samples_leaf=10.

result = permutation_importance(

rf, X_train, y_train, n_repeats=10, random_state=42

)

sorted_idx = result.importances_mean.argsort()

fig, ax = plt.subplots()

ax.boxplot(

result.importances[sorted_idx].T, vert=False, labels=X_train.columns[sorted_idx]

)

ax.set_title("Permutation Importances (train set)")

fig.tight_layout()

plt.show()

Regularization Methods Example 5.2¶

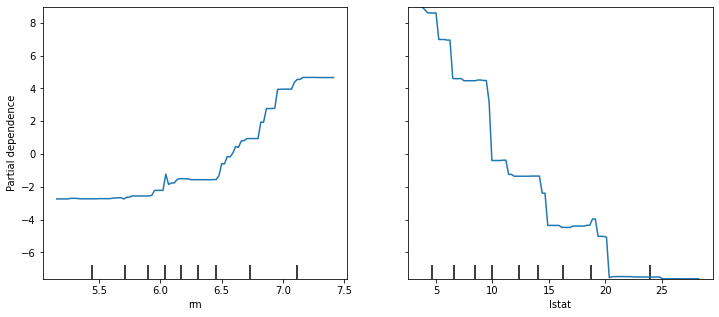

In example 4.1 we saw that lstat and rm are by far the most important variables. We can also produce partial dependence plots for these two variables.

import pandas as pd

import numpy as np

from sklearn.model_selection import train_test_split

from sklearn.ensemble import GradientBoostingRegressor

# Load data

df = pd.read_csv('Regularization Techniques/data/Boston.csv', index_col=0)

# Define target and predictors

x = df.drop(columns='medv')

y = df['medv']

# Split in test and train set

np.random.seed(1)

x_train, x_test, y_train, y_test = train_test_split(x, y,

test_size=0.5)

# Fit model:

reg = GradientBoostingRegressor(n_estimators=5000, max_depth=4,

learning_rate=0.001)

reg = reg.fit(x_train, y_train)from sklearn.datasets import make_regression

from sklearn.ensemble import GradientBoostingRegressor

from sklearn.inspection import plot_partial_dependence

import matplotlib.pyplot as plt

import pandas as pd

# Plotting partial dependence

fig = plt.figure(figsize=(12, 5))

ax = fig.add_subplot(1, 1, 1)

plot_partial_dependence(reg, x_train, ['rm', 'lstat'], ax=ax, kind='average')

plt.show()

These partial dependence plots illustrate the marginal effect of the selected variables on the response after integrating out the other variables. In this case, as we might expect, median house prices are increasing with rm and decreasing with lstat.